July Market Update 2026

This month, we discuss the Fed's closer-than-expected hold, the bear-steepening it triggered, and the forced deleveraging that amplified an AI-driven selloff.

While India heads to the polls, elections are one factor investors in China do not have to consider. But plenty of other challenges have weighed on Chinese stocks, which have retreated heavily in the last three years in the face of domestic and geopolitical risk, a limp post-COVID recovery, an ongoing real estate crisis and an attempted restructuring of the economy towards a new growth model. A lot of negatives are already priced in to Chinese equities. Valuations are steeply discounted compared to other markets and Chinese stocks’ own history. This suggests limited further downside and a possibly convex opportunity for tactical gains – especially if a catalyst can be found for a rebound, likely in the shape of more meaningful government stimulus.

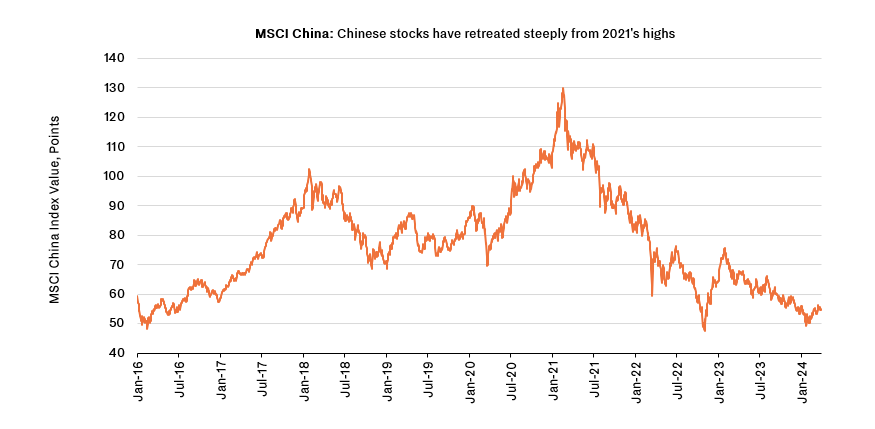

Chinese equities have heavily underperformed in recent years.

Chinese equities have suffered three back-to-back years of double-digit falls. Following an -11% calendar year decline, by the end of 2023 the blue-chip onshore CSI 300 Index was down -42% from its 2021 peak. The slump was even worse for offshore stocks. (The universe of Chinese equities includes A-Share listings on the Chinese mainland, offshore H-Share listings in Hong Kong, as well as listings in New York and elsewhere.) The broad MSCI China Index, covering both onshore and offshore stocks, was down -55% over the same period. These reversals have even taken Chinese indices below their 2019, pre-COVID levels to five-year lows. Overseas investors have headed for the exit, with global portfolios’ allocations to China dropping to decade lows.

A well-known litany of economic problems – including weak consumer demand and property sector travails – have pushed Chinese stocks down. The mood music on the Chinese economy has become almost universally glum.

The economic challenges dragging on Chinese equities are by now well known. The scarring from heavy, extended coronavirus restrictions has not been healed by a post-reopening recovery that has largely fizzled out. GDP growth is well down from the dizzying heights of the pre-pandemic era and deflation has set in. Animal spirits – especially amongst Chinese consumers – remain in the doldrums, pulled lower by an ongoing real estate crisis. The property sector’s difficulties were set off by deliberate government efforts to deflate a bubble and force the sector to deleverage. But the sector’s vast size – it is connected to around a third of GDP value creation – and centrality to China’s growth model since the financial crisis mean its weakness is dragging on the whole economy. Amongst other things, it has exposed heavily leveraged Chinese local governments’ weak financial position, as China faces a ‘great wall of debt’.

Chinese stocks have also been hit by domestic and geopolitical risk. Heavy-handed regulatory intervention by Beijing – most strikingly with the overnight termination of the for-profit education services industry – has rightly spooked investors. Meanwhile, tensions with the US have ratcheted up and both the Trump and Biden administrations have taken concrete action impacting the Chinese economy – including hindering its access to high-level technology.

Amidst all these difficulties, negative sentiment towards the Chinese economy, both at home and abroad, has become consensus – and near universal – a possible contrarian indicator.

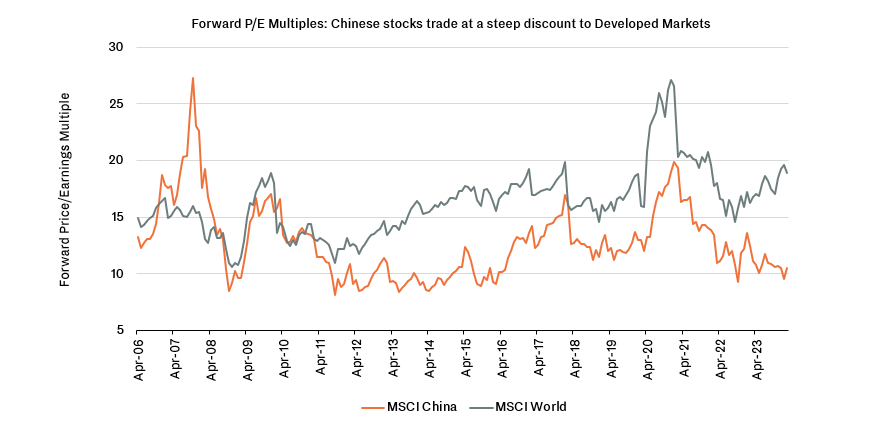

A lot of negatives are already priced in, leaving valuations deeply depressed.

These difficulties are both well known and heavily priced into Chinese stocks. The blue-chip onshore CSI 300 Index trades at a P/E ratio of 11.4x. The wider Chinese equity universe is even cheaper; the MSCI China’s forward P/E ratio measures 8.9x. This marks a discount not only to other emerging markets (the MSCI EM ex-China’s forward P/E ratio is at 14x) but is steeply cheaper than developed markets. The MSCI World Index’s forward P/E is 18.9x, while the S&P 500 is at 21.1x.

With sentiment so negative on Chinese stocks, this naturally raises the contrarian question: how much more downside could there be at these levels?

Beijing policymakers are resisting investor hopes of a ‘big bazooka’ stimulus – but prospects for more government support are growing.

Investors at home and abroad are watching eagerly for major government stimulus to kick the economy back into gear and trigger a stock-market rally off the currently low levels. However, policymakers have been resisting any ‘big bazooka’ stimulus akin to the vast 2008-9 infrastructure spending package. Although that earlier stimulus successfully protected China’s economy from the 2008 global financial crisis, Beijing policymakers also see it as a source of many of China’s current problems, including excessive leverage and unproductive infrastructure investments – and are therefore keen to avoid any straightforward repeat.

Instead, stimulus has so far been low-key and incremental. The People’s Bank of China (PBoC), the central bank, has gradually trimmed interest rates, most recently cutting the five-year Loan Prime Rate (the key mortgage benchmark) by 25 basis points, the largest cut yet. But the PBoC is only willing and able to go so far in a context of high developed-market yields, especially in the US (meaning deeper rate cuts could accelerate capital flight). The PBoC has also reduced banks’ reserve requirements, in an effort to loosen credit flows.

On the fiscal side, meanwhile, government support has largely been confined to rhetoric so far. However, that has recently begun to shift. At the annual meeting of China’s rubber-stamp parliament, premier Li Qiang announced issuance of 1 trillion renminbi ($139bn) of ultra-long-term special treasury bonds to bridge funding shortages and advance major projects. However, there were no specific details of how the proceeds will be used. And whilst announcing the issuance, Li told all levels of government they would ‘have to keep their belts tightened’ – indicating no wholesale move to throw money at the problem.

Beijing is right to tread cautiously. It does not have unlimited fiscal room and the Chinese economy needs to deleverage – not risk adding more unproductive liabilities with potentially unproductive investments. The shift from an infrastructure and property-driven model, aiming at simply maximising headline GDP growth figures, is appropriate at China’s current stage of development. Nonetheless, the pressure on policymakers to reinvigorate animal spirits is real – including to support equity markets. Approximately 200mn Chinese people own stocks – principally the urban middle classes. This is a constituency the Chinese Communist Party can ill afford to alienate. Beijing is sensitive to the need to boost stocks off their current lows. At the very least, policymakers are determined to put a floor under Chinese equities. Since the Lunar New Year holiday, Beijing has deployed the so-called ‘National Team’ of state-owned financial entities to buy up Chinese stocks. The result has been a +13% rally for the CSI 300 from February’s low point.

The Chinese economy retains real strengths. Deeply discounted Chinese stocks may offer a convex opportunity.

For now, Chinese stocks at deeply depressed valuations represent a tactical opportunity. Booming AI champion NVIDIA’s market cap now exceeds that of all Hong Kong-listed Chinese H-Shares – hardly commensurate with the scale and potential of the world’s second-largest economy, even as it struggles with a notch down in its growth. Policymakers are looking to reorientate the economy away from the GDP-gains-at-all-costs approach of earlier eras and now emphasise ‘high-quality development’, with a greater emphasis on higher tech, future leading industries, and national economic security. It is not clear that they have a comprehensive plan to deliver on all this – and the current transition is creating uncertainty.

But the Chinese economy retains real strengths, that also spill into its equity markets. Chinese players are increasingly clear leaders in electric vehicles, batteries and other clean tech – all areas with strong global demand runways. Some in the Chinese internet space – hit hard in recent years – are finding international success, such as Schein and Pinduoduo (through its global platform, Temu). Domestic consumer demand may be muted but the recent Lunar New Year holiday saw it trending up, and Chinese consumers sit on large savings piles. They also increasingly favour homegrown brands, meaning domestic equities are the best place to gain exposure to a recovery of animal spirits. Chinese shares have plumbed similar valuation depths on four previous occasions in the last 20 years. On each occasion they benefited from strong tactical recoveries, generating between +39% and +88% of equity returns from trough to peak. Downside risks remain; for example, China policy may become a political football in the approaching US presidential election. But geopolitical headwinds are already heavily priced in. With expectations now so low, the opportunity looks convex.

Click here to go back to Asia Overview

If you would like to find out more about this theme or how you can take advantage of the current climate, please get touch with info@bedrockgroup.ch.

Authored by:

Important Legal Information

The content of this document has been prepared by Bedrock S.A., Bedrock Monaco SAM, and Bedrock Asset Management (UK) Ltd. (jointly, hereafter, “Bedrock”).

The information and opinions contained in this document are for background information and discussion purposes only and do not purport to be full or complete. No information in this document should be construed as providing financial, investment or other professional advice.

The information contained herein is intended for the sole use of the recipient and may not be copied or otherwise distributed or published without the express consent of Bedrock. Although the information contained herein has been established by Bedrock based on or by reference to sources, documents and systems it believes to be reliable and accurate, Bedrock does not guarantee its accuracy or completeness and assumes no responsibility for any losses that may arise from the use of this information.

Information included in this document is intended for those investors who meet the definition of Professional Client under the Swiss FinSA regulation as well as Professional Client or Eligible Counterparty under the UK Financial Conduct Authority.

Confidentiality

This presentation and the information contained herein are confidential. Each copy of this presentation is addressed to a specifically named recipient and shall not be passed on to a third party. By its acceptance hereof, the recipient agrees to keep the presentation and its contents strictly confidential and may not disclose or divulge any information contained herein to any other person. This presentation cannot be published, copied, reproduced or distributed in any manner whatsoever. The recipient will use this presentation for the sole purpose of obtaining a general understanding of the business, operations and financial performance of Bedrock in order to make a decision as to whether the recipient should proceed with a further investigation of the Funds and this investment opportunity. Bedrock reserves the right to request the return of this presentation at any time, without the retention of any copies by the prospective investor.

Investment Risks The value of all investments and the income derived therefrom can fluctuate due to market movements and you may not get back the amount originally invested. In the case of overseas investments, values may vary as a result of changes in currency exchange rates. This may be due, in part, to exchange rate fluctuations in investments that have an exposure to currencies other than the

base currency of the portfolio. Past performance is no guide to or guarantee of future performance.

Limitation of Liability and Indemnity

Bedrock expressly disclaims liability for errors or omissions in the information and data contained in this document. No representation or warranty of any kind, implied, expressed or statutory, is given in conjunction with the information and data. Bedrock accepts no liability for any loss or damage arising out of the use or misuse of or reliance on the information provided including, without limitation, any loss of profits or any other damage, direct or consequential. You agree to indemnify and hold harm less Bedrock and its affiliates, and the directors and employees of Bedrock and its affiliates from and against any and all liabilities, claims, damages, losses or expenses, including legal fees and expenses arising out of your access to or use of the information in this presentation, save to the extent that such losses may not be excluded pursuant to applicable law or regulation. Any opinions contained in this presentation may be changed after issue at any time without notice.

Copyright and Other Rights

The copyright, trademarks and all similar rights of this presentation and the contents, including all information, graphics, code, text and design, are owned by Bedrock.

This month, we discuss the Fed's closer-than-expected hold, the bear-steepening it triggered, and the forced deleveraging that amplified an AI-driven selloff.

Emerging market equities have delivered strong performance in 2026, fuelled by surging demand for AI-related technologies and significant gains across North Asian markets. In this article, Bedrock's Head of Investment Advisory, Helena Eaton, explores the key drivers behind this rally and the opportunities that may lie ahead.

This month we discuss an Iran ceasefire that finally won its signatures and the oil unwind that followed, Kevin Warsh’s first meeting at the Fed and the real-rate squeeze it set off, a blockbuster SpaceX debut that soared then drifted, and a memory shortage that turned an Asian semiconductor selloff into a story about demand, with a change of government in Britain and the ECB’s first hike in two years rounding out a busy month.