July Market Update 2026

This month, we discuss the Fed's closer-than-expected hold, the bear-steepening it triggered, and the forced deleveraging that amplified an AI-driven selloff.

India – now not just the world’s largest democracy but also its most populous country – goes to the polls next month. International investors, increasingly drawn into the country’s stock markets by a compelling growth story, will be watching closely. Seeking re-election for a third term, Prime Minister Narendra Modi must fancy his chances. The opposition is divided and diminished – but perhaps most importantly, the election comes as the country basks in its status as the fastest growing major economy, and its stock markets enjoy a period of rapid gains. Per capita GDP has more than doubled since Modi came to power in 2014. Modi’s brand of digitally savvy, pro-business nationalism looks set to continue in power after results are announced in June. The question for investors, therefore, is above all: how much growth is there to come – and how much has been priced in already?

India’s economy is surging, giving Indian stocks a solid fundamental base – with plenty of runway for further growth.

Indian stocks are backed by arguably the most compelling macroeconomic story of any major economy right now. India is climbing the global ranks. The IMF expects it to overtake Germany and Japan to become the world’s third largest economy (in nominal GDP terms) by 2027. From 2014 to 2022, compound annual GDP growth averaged +5.6%. In 2023, India was the fastest growing major economy, with YoY growth ratcheting up to +8.4% in Q4. Exports of goods and services are on track to swell around +17% YoY in the fiscal year ending this month. And the country looks set to maintain the positive momentum. The IMF forecasts it will chalk up +6.5% growth in both 2024 and 2025.

Prime Minister Modi is therefore perhaps not wrong to have declared that India has entered amrit kaal, the Vedic ‘time of nectar’.

More prosaically, these strong macroeconomic fundamentals are feeding through to Indian equities, including via earnings growth for listed companies. And there is plenty more runway for further growth. India might be getting richer at a rapid clip – but it is still a poor country. Its GDP – both in aggregate and per capita – is a fraction of China’s (specifically, it is around one-fifth of its rival Asian giant, by both measures).

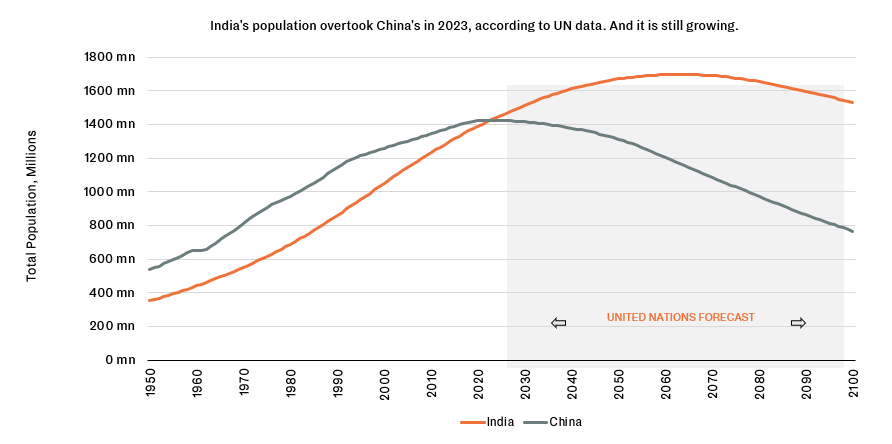

Now the largest on earth, the growing population is young, urbanising and increasingly wealthy.

A key dimension of India’s growth trajectory is demographic. Last year, India overtook China to become the most populous nation on earth. And whereas China’s population is shrinking and ageing, India’s remains youthful and (according to UN data) growing. India faces the boon of an expanding working-age population. Labour will remain plentiful and the dependency ratio shrinking. That labour is still competitively priced: Indian wage costs are only a fifth of China’s and two-fifths of Vietnam’s.

India’s burgeoning working population may be comparatively cheap but Indians are moving up the income ladder, adding ever more to the country’s appeal as a massive consumer market. Absolute poverty is declining (but is still a grim reality) and the ranks of India’s middle classes are swelling. Definitions of this bracket vary widely; so, consequently, do estimates of its size. But three things are clear: it numbers in the hundreds of millions, it is growing, and so is its spending power. Some estimates suggest India will account for 40% of global middle class consumption by 2050, up from around 5% now.

Government policy – at both national and state level – is providing meaningful support, including business-friendly reforms, pro-growth programmes and infrastructure investment.

The government is not leaving growth up to demographic chance. Though Indian bureaucracy may in many ways still deserve its reputation as a ponderous burden, the picture is improving. Indeed, the country has raced up the World Bank’s Ease of Doing Business ranks, reaching 63 in 2020, up from 142 just five years earlier. The government is making a positive contribution, both through changing regulations and fiscal action.

Modi has vowed to make India a developed economy by 2047, the centenary of its independence. On coming to power in 2014, he launched the Make in India campaign, aimed at building out India’s role in global manufacturing. His government has pursued business-friendly, pro-growth measures, such as corporate tax cuts and a revised bankruptcy code. A key development was the simplification of a patchwork of taxes into a nationwide goods and services tax, making the continent-sized country more of a single market. Also transformative has been the digitisation of government and economy, through the ‘India Stack’ decentralised digital infrastructure. Digitisation has boosted formalisation of the economy and eased access to services, including banking.

Modi gets plenty of the credit for the changes of the last decade – and seems poised to do so in the upcoming general elections – but the role of India’s powerful state governments should not be neglected (they control 60% of government spending, after all). State-level reforms are proving key in India’s economic development, with particularly business-friendly states like Gujarat, or Tamil Nadu and Karnataka in the south leading the way. The latter has reformed its labour laws to move in line with working practices in China in order to attract manufacturers like Apple supplier Foxconn; maximum shifts have increased from 9 hours to 12 and the rules on night-time work have been eased, paving the way for 24-hour, two-shift production.

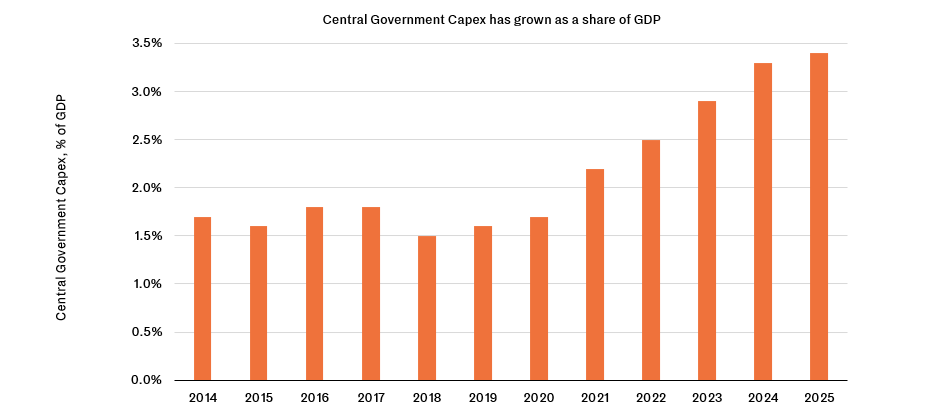

Also echoing the Chinese experience, massive, government-led infrastructure investment is spurring India’s investment cycle and giving the economy both direct and indirect boosts. In its final pre-election budget, Modi’s government announced $134bn on infrastructure building, a +11% increase YoY. This rate of growth was actually more modest than in recent years; it grew at +27% annualised over the last four years. Capital expenditure as a share of GDP has swiftly climbed above 3%, from under 2% in 2019-20. Spending on roads, railways and airports is at record levels. India has added 10,000km of roads annually since 2018. This has a significant multiplier effect, adding to aggregate demand and facilitating economic activity. It is also feeding into an accelerating investment cycle. Residential construction is growing as the country urbanises and corporate capex is trending higher. Capacity utilisation rates are high, encouraging more investment in productive capacity to meet demand. All in all, though, India’s capital stock remains very low, both per worker and as a share of GDP, suggesting there is much more capital formation to come – meaning more investment across the economy.

Finally, the macroeconomic framework is on a stable footing. At 87%, the debt-to-GDP ratio is high but not dramatically so. The government is consolidating its finances to trim the fiscal deficit to 5.1% in the coming fiscal year. The Reserve Bank of India, the central bank, is maintaining effective oversight – latterly avoiding runaway inflation. The banking system more widely is in good health.

Indian equities have made strong gains in recent years, leaving valuations comparatively rich. However, they do not appear drastically overpriced compared to other markets, or their own history. A valuation premium can be justified if India’s growth trajectory holds.

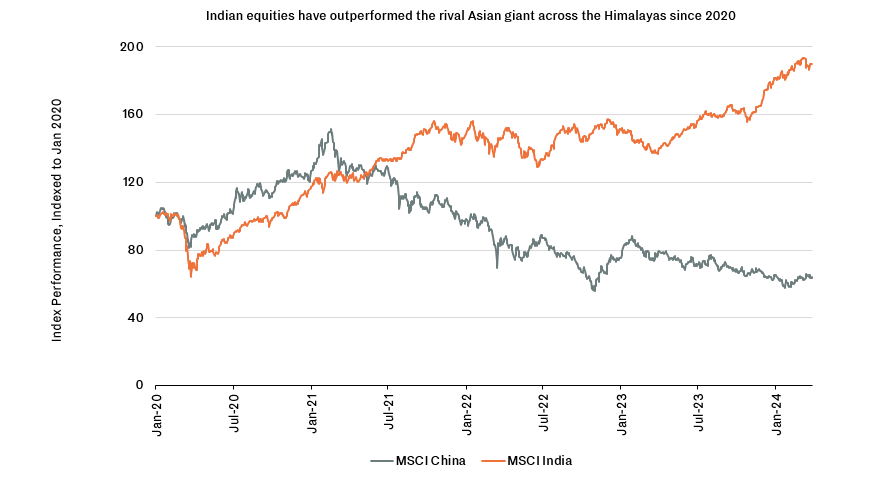

India’s strong growth story has not been lost on markets. The blue-chip Sensex Index is up a cool +75.7% since the start of 2020. The broader MSCI India Index gained +67.1% in dollar terms over the same period. After a muted 2022, gains accelerated in 2023 as the MSCI India gained +22%.

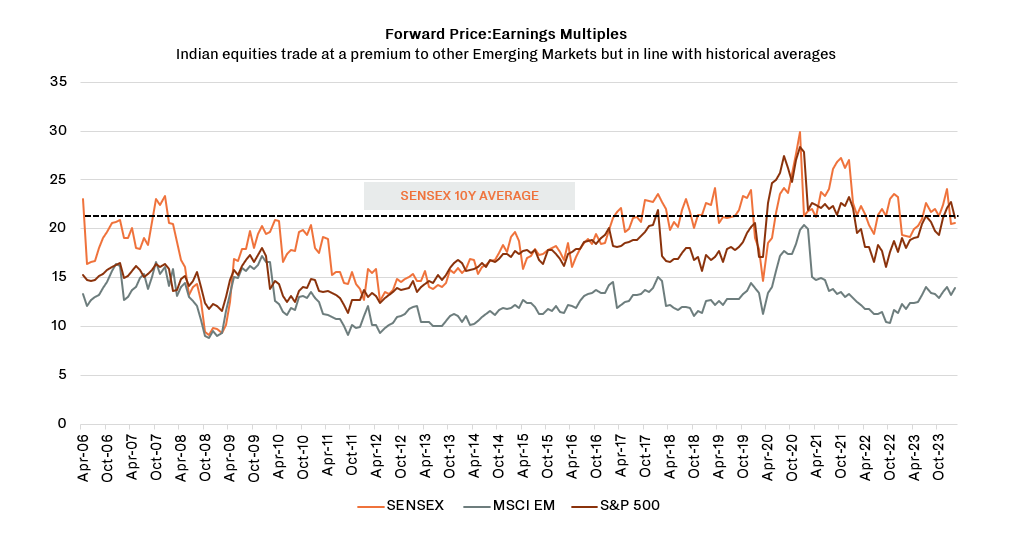

In the wake of these gains, a lot of the country’s growth story is priced in. The Sensex trades at a trailing P/E of 23.0x and a forward P/E of 20.6x. The equivalent figures for the MSCI India are 27.0x and 22.9x, respectively. This puts it well ahead of the wider emerging market universe (the MSCI EM Index’s trailing P/E is 15x and its forward P/E 14x) and in line with the S&P 500’s 24x (trailing) and 21x (forward).

Comparatively rich valuations have long been a recurring feature of Indian equities – the question is what price can be justified by expected future growth. Indian valuations are at a premium to certain other markets, to be sure – but not staggeringly so. The Sensex’s P/E ratios today are almost exactly in line with their 10-year averages – they are in fact slightly lower. Indeed, current valuations are in fact cheaper now than they were between 2020 and 2022, despite 2023’s rally. You have to go back to 2015 to see meaningfully cheaper valuations – and the growth outlook has strengthened markedly since then. Indian stocks’ valuations can be justified … if India’s current growth trajectory can hold.

The sustainability of India’s growth trajectory cannot be guaranteed – and there are weaknesses in its performance, from high unemployed and low female labour-force participation, to a still-small manufacturing sector. A protectionist instinct amongst policymakers remains a threat to India’s emergence as a competitive global player.

Modi claims Indians will now drink the nectar of amrit kaal. But triumphalism would be premature. For all its strengths, India still has a long road ahead of it – especially if it is to reach the ambitious goal of becoming a developed economy by its centenary year. To do so, GDP will need to sustainably grow 6-7% annually. That is by no means guaranteed – and there are real gaps in India’s performance so far.

Much of the current focus on India from market participants and commentators centres on its prospects as ‘the next China’ – another Asian giant achieving stunning growth over decades by becoming a workshop of the world. Indeed, New Delhi’s economic policy (notably Make in India) looks for India to emerge as a major manufacturing power. But progress has been limited – and, for better or worse, India’s economy looks very different from China’s, either now or at the start of its take-off. India’s is a private consumption driven economy (representing c.60% of GDP), rather than export-driven. Where it is plugged into global markets, it is above all in services, rather than goods exports. Manufacturing sector growth rose into double digits in 2023 in dollar terms. However, it remains comparatively small as a share of the total economy, at 13% value added to GDP; compare that with 28% for China, or indeed 25% for Vietnam and 19% for Indonesia. (The US figure is 11%.) Over the last decade, rising wage costs have seen China shed global market share in labour-intensive goods. India has only picked up a fraction of this – losing out to the likes of Bangladesh and Vietnam. Manufacturing’s share of the economy is in fact down from 17% in 2010.

Related to this, employment remains a challenge. A demographic boom only pays dividends if it can be employed. Unemployment in the 15-34 age bracket stood at 45.4% in 2023 – and 10% for the full population. The picture has scarcely improved in Modi’s decade in power. Women are underrepresented in the workforce. International Labour Organisation data put female labour force participation as low as 28% – below neighbour Bangladesh (37%); lower, even, than Saudi Arabia (34%). It is well behind the likes of Vietnam (69%) and China (61%), where female labour has been crucial to the labour-intensive, light industries (including textiles and electronics assembly) that have historically launched industrial take-off.

Such industries have been a blind spot for New Delhi policymakers. Industrial policy campaigns like Make in India have tended to focus more on capital-intensive sectors such as mobile phones and pharmaceuticals – that boast higher prestige but fewer jobs. A protectionist instinct does not help. Tariffs and tighter rules of origin mean that whereas foreign inputs represented c.40% of exports in Vietnam and China’s early textile-led take-offs, the equivalent for India today is just 16%. In this way, India manufacturing struggles to compete internationally. The government shocked markets last year when it announced immediate imposition of new licence requirements for the import of tech products such as tablets and PCs. Following a backlash, the move was watered down – but still pointed to the risk of retrogression towards the protectionist ‘Licence Raj’ chipped away by the 1990s reforms. Modi talks of an Atmanirbhar Bharat – a self-reliant India – that is at first glance difficult to distinguish from the old swadeshi (self-sufficiency) movement.

For now, India remains the poorest of the BRICS countries and a long way off its goal to attain developed-economy status. The positive take is there is a long runway of further (potentially rapid) growth. The negative version is this will be difficult – and there have been false dawns before. However, the present moment offers an encouraging alignment of macroeconomic fundamentals, supportive policy and a largely positive geopolitical environment.

For now, India remains the poorest of the BRICS countries and a long way off its goal to attain developed-economy status. The positive take is there is a long runway of further (potentially rapid) growth. The negative version is this will be difficult – and there have been false dawns before. However, the present moment offers an encouraging alignment of macroeconomic fundamentals, supportive policy and a largely positive geopolitical environment. An important driver of international investors’ interest in Indian equities in recent years has been growing tension between China and the US and a wider drive by multinationals to diversify supply-chains, of which India may be one beneficiary. This trend looks set to continue in the foreseeable future.

India’s economy might face challenges – but not all of these need matter to investors in Indian equities (even if weaknesses like low female labour-force participation equate to opportunities squandered). Indeed, corporates’ strong share of recent growth – a concern in some quarters – is a positive for shareholders. Indian stocks’ valuations appear justifiable in the face of the most promising growth opportunity of any major economy. The outcome of the upcoming massive, seven-stage election may stimulate further international in-flows into India’s stock markets.

Click here to go back to Asia Overview

If you would like to find out more about this theme or how you can take advantage of the current climate, please get touch with info@bedrockgroup.ch.

Authored by:

Important Legal Information

The content of this document has been prepared by Bedrock S.A., Bedrock Monaco SAM, and Bedrock Asset Management (UK) Ltd. (jointly, hereafter, “Bedrock”).

The information and opinions contained in this document are for background information and discussion purposes only and do not purport to be full or complete. No information in this document should be construed as providing financial, investment or other professional advice.

The information contained herein is intended for the sole use of the recipient and may not be copied or otherwise distributed or published without the express consent of Bedrock. Although the information contained herein has been established by Bedrock based on or by reference to sources, documents and systems it believes to be reliable and accurate, Bedrock does not guarantee its accuracy or completeness and assumes no responsibility for any losses that may arise from the use of this information.

Information included in this document is intended for those investors who meet the definition of Professional Client under the Swiss FinSA regulation as well as Professional Client or Eligible Counterparty under the UK Financial Conduct Authority.

Confidentiality

This presentation and the information contained herein are confidential. Each copy of this presentation is addressed to a specifically named recipient and shall not be passed on to a third party. By its acceptance hereof, the recipient agrees to keep the presentation and its contents strictly confidential and may not disclose or divulge any information contained herein to any other person. This presentation cannot be published, copied, reproduced or distributed in any manner whatsoever. The recipient will use this presentation for the sole purpose of obtaining a general understanding of the business, operations and financial performance of Bedrock in order to make a decision as to whether the recipient should proceed with a further investigation of the Funds and this investment opportunity. Bedrock reserves the right to request the return of this presentation at any time, without the retention of any copies by the prospective investor.

Investment Risks The value of all investments and the income derived therefrom can fluctuate due to market movements and you may not get back the amount originally invested. In the case of overseas investments, values may vary as a result of changes in currency exchange rates. This may be due, in part, to exchange rate fluctuations in investments that have an exposure to currencies other than the

base currency of the portfolio. Past performance is no guide to or guarantee of future performance.

Limitation of Liability and Indemnity

Bedrock expressly disclaims liability for errors or omissions in the information and data contained in this document. No representation or warranty of any kind, implied, expressed or statutory, is given in conjunction with the information and data. Bedrock accepts no liability for any loss or damage arising out of the use or misuse of or reliance on the information provided including, without limitation, any loss of profits or any other damage, direct or consequential. You agree to indemnify and hold harm less Bedrock and its affiliates, and the directors and employees of Bedrock and its affiliates from and against any and all liabilities, claims, damages, losses or expenses, including legal fees and expenses arising out of your access to or use of the information in this presentation, save to the extent that such losses may not be excluded pursuant to applicable law or regulation. Any opinions contained in this presentation may be changed after issue at any time without notice.

Copyright and Other Rights

The copyright, trademarks and all similar rights of this presentation and the contents, including all information, graphics, code, text and design, are owned by Bedrock.

This month, we discuss the Fed's closer-than-expected hold, the bear-steepening it triggered, and the forced deleveraging that amplified an AI-driven selloff.

Emerging market equities have delivered strong performance in 2026, fuelled by surging demand for AI-related technologies and significant gains across North Asian markets. In this article, Bedrock's Head of Investment Advisory, Helena Eaton, explores the key drivers behind this rally and the opportunities that may lie ahead.

This month we discuss an Iran ceasefire that finally won its signatures and the oil unwind that followed, Kevin Warsh’s first meeting at the Fed and the real-rate squeeze it set off, a blockbuster SpaceX debut that soared then drifted, and a memory shortage that turned an Asian semiconductor selloff into a story about demand, with a change of government in Britain and the ECB’s first hike in two years rounding out a busy month.