July Market Update 2026

This month, we discuss the Fed's closer-than-expected hold, the bear-steepening it triggered, and the forced deleveraging that amplified an AI-driven selloff.

On Thursday 22nd February 2024, Japanese stocks made history – by repeating the past. After a long, long wait, Tokyo’s Nikkei 225 Index finally regained the all-time-high it first attained on the final day of 1989. In 1990 Japan’s so-called ‘Bubble Economy’ burst and the country – and its stock market investors – endured lost decades. This much delayed stock market recovery has come on the back of more than a year of strong gains for Japanese equities, as overseas investors reappraised the country’s offering. And the Nikkei – and other key indices – have continued on to new heights.

Another historic day followed swiftly as the Bank of Japan (BoJ) in March began to dismantle its unorthodox, ultra-dovish monetary policy. There are signs the deflationary torpor of the lost decades is finally lifting. With the post-COVID economic recovery holding, the outlook for Japan is looking brighter than for some time. Japanese equities hold considerable value – which finally looks poised to be unlocked.

Japanese equities have enjoyed more than 12 months of strong gains as the macroeconomic picture has brightened, allowing them to strike new all-time-highs.

Japanese equities were Asia’s top performers in 2023 – and have carried the positive momentum into 2024. The Nikkei 225 rose +28% in 2023 and has added a further +21% YTD. The broader TOPIX Index gained +25% and +17% in the same periods, respectively. Since overhauling that 34-year-old all-time-high of 38,915, the Nikkei 225 has marched higher, crossing the 40,000-point threshold. After long years out of favour, Japanese markets attracted $43.4bn of net foreign inflows in 2023, the largest influx since at least 2014. A cheap yen has helped burnish the appeal of Japanese stocks, as has a healthy (if not breakneck) recovery from Japan’s COVID restrictions, the last of which were lifted in 2023.

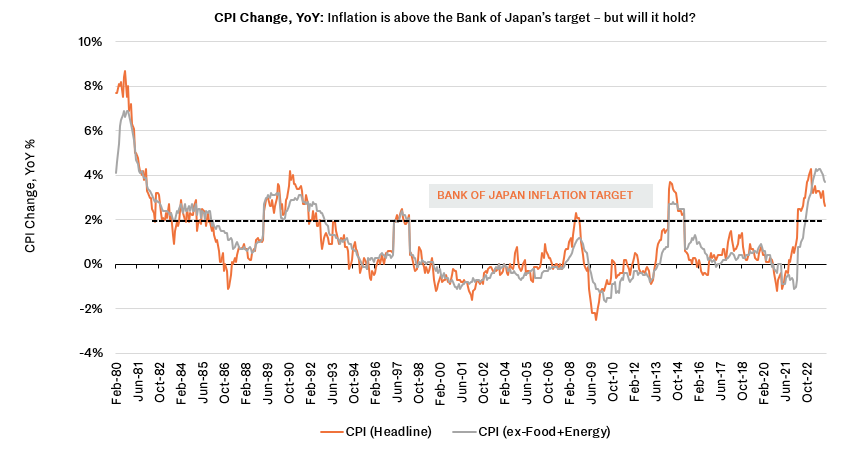

Inflation is holding at or above the Bank of Japan’s target, as companies finally pass on cost rises to consumers, and workers secure rising wages. This has allowed the Bank of Japan to at last begin to tighten – and normalise – monetary policy. Japan may at last be back on a path to macroeconomic normality after its deflationary lost decades.

Japan appears finally to be turning a page on an era of ultralow inflation (or outright deflation) and negative interest rates. In an eagerly anticipated move, the BoJ in March made its first interest rate hike in 17 years – taking policy rates out of negative territory and into a 0-0.1% target range. At the same time, it ended its Yield Curve Control (YCC) policy. In place since 2016, YCC is an unorthodox monetary tool aimed at pinning the sovereign yield curve at chosen points – backed by massive central bank purchases. The BoJ had employed YCC in an effort to stimulate the economy and revive price growth back to the Bank’s 2% inflation target.

A deflationary mindset – in which expectations for falling prices stymie growth – was a hallmark of Japan’s lost decades. Ending it is crucial to returning Japan to sustainable economic growth. Whereas the pandemic-era bout of inflation was an unwelcome blast from the past for most developed countries, and one to be battled back, it was embraced as an opportunity by Japanese policymakers. If anything, they fear it will not hang around long enough. Similarly, most central bankers fear a so-called ‘wage-price spiral’ (where workers respond to price rises by demanding greater nominal pay increases to maintain their economic position – but ultimately push prices higher, causing inflation to run out of control) but the BoJ has been pushing for a – virtuous – spiral to set in.

Indications suggest their wish may be coming true. Headline inflation peaked above 4% YoY in 2023. Crucially, what began – as elsewhere – as imported inflation initially sparked by supply-chain disruptions and spiking energy prices, has showed signs of bedding in domestically. While it has cooled somewhat, core inflation is so far holding above the BoJ’s 2% target. Data indicate Japanese companies are finally passing on rising costs to consumers. And most importantly, wage growth is finally reviving. Backed by policymakers (and even parts of corporate Japan), trade unions have secured their largest pay increases in decades. In the latest shunto spring wage negotiation rounds, workers at large companies secured average gains of +4%, the highest since 1992.

The seeming return to a healthier state of price growth and positive interest rates is giving Japanese equities a key fundamental boost, suggesting corporate earnings may trend up.

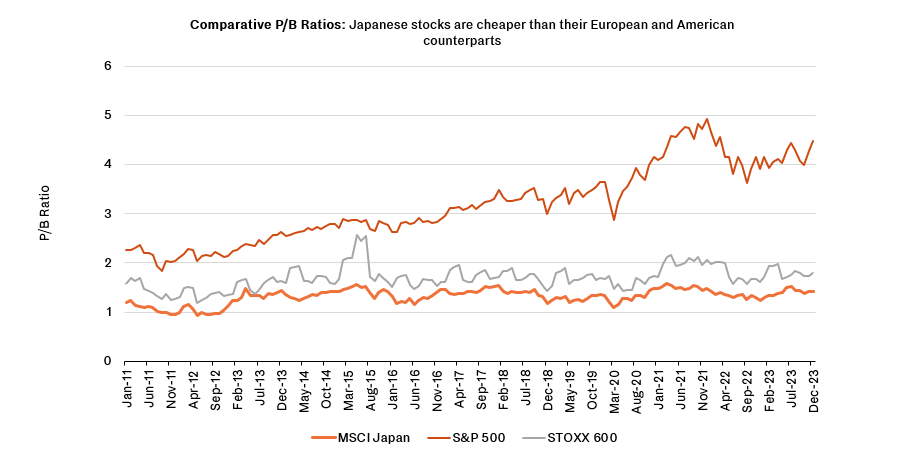

Japanese stocks have long been cheap on a relative basis. Revitalised governance reforms are beginning to unlock their pent-up value.

Japanese equities have long been cheap by key equity valuation metrics, relative to counterparts elsewhere. Even with the gains of the last year, the MSCI Japan Index trades at a 15.7x price to forward earnings multiple, compared to 18.3x for the MSCI World and 21.2x for the S&P 500. But it is relative to their net assets that Japanese stocks really stand out as underpriced. The MSCI Japan trades as a price-to-book ratio (P/B) of 1.6x, a steep discount relative to 3.3x for the MSCI World and 4.9x for the S&P 500. By 2023, half of all stocks on the Tokyo Stock Exchange’s Prime Market traded at a P/B below 1.0 … which is to say that the market valued these companies less than the assessed book value of their assets.

A primary explanation is that the denominator in that P/B ratio – companies’ net assets – is, in many cases, so outsized. Many Japanese firms sit on bloated balance sheets featuring relatively unproductive assets, including large cash hoards. (According to one analysis, 49% of Japanese companies’ net assets was cash.) But the cause underlying this is a corporate culture that has not historically favoured shareholder value creation. Company managements have felt little pressure to either redeploy capital more efficiently, or return it to shareholders (for example via share buybacks). More widely, unsolicited takeover bids have been taboo in corporate Japan, impeding mergers and acquisitions that could otherwise hasten redeployment of capital.

Policymakers and regulators have long sought to shift these dynamics and boost corporate value creation – and, with it, the stock market. They stepped up their efforts last year. Market regulator Japan Exchange Group instructed companies trading below 1.0 P/B to submit value creation plans, setting out actions they would take to drive their P/Bs up. Failure to submit plans would result in naming and shaming via a monthly updated list. The regulator has also suggested that companies that fail to make progress on valuation could be delisted.

This redoubled pressure appears to be bearing fruit, alongside other reforms begun under former prime minister Abe Shinzo to push for better corporate governance and more efficient use of capital. Managements are showing more willingness to deploy their assets. Capital investment rose in 2023. Unsolicited takeover bids also trended up, eroding the long-standing taboo as corporate leaders looked to seize value creation opportunities. Share buybacks, too, picked up markedly in 2023.

A doubled tax-free investment allowance for Japanese savers adds another potential near-term catalyst.

Another possible impulse for Japanese stocks could come from the country’s own retail savers. According to the BoJ, Japanese citizens are sitting on a vast $7.7tn cash pile – but have a very low rate of equity investments. Their ¥2.1 quadrillion of cash and deposit holdings equate to the combined annual GDP of India and Germany. Only 13% of Japanese households’ liquid assets are in stocks, in contrast to over 40% in the US and 21% in Europe. One reason for this is the psychological overhang of the Nikkei’s long trough – 34 years before breakeven would weigh on most investors. Japanese markets’ renewed vitality may finally lift the shadow and tempt more domestic savers back in.

A more tangible factor may also help. Changes to the Nippon Individual Savings Account (NISA) have come online this year. Retail investors’ annual tax-free investment allowance has been doubled to ¥2.4mn (c.$16,200) and the lifetime maximum tax-free investment allowance for equity investments increased to ¥18mn (c.$122,000). A new Growth Investment NISA has also been created for equity investments. In the first month of the revamped system, $9.3bn of new NISA capital flowed into equity funds. The NISA does not stipulate investment in Japanese assets – and initial evidence points to a sizeable portion of new NISA inflows heading to overseas markets – but even a minority of NISA assets could add an important new bid for Japanese equities.

The Japanese economy’s recovery from the deflationary lost decades is not guaranteed – but Japanese equities are well placed to unlock further value.

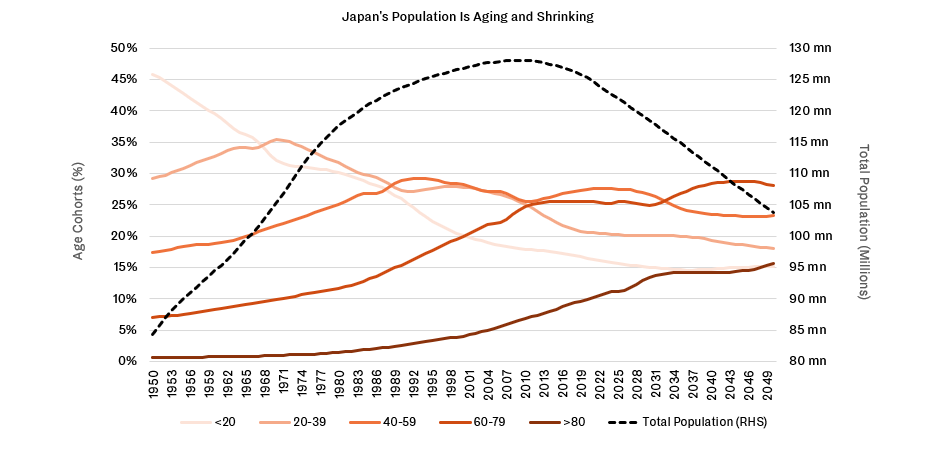

Japanese equities have already made considerable ground over the last year – and further progress is not a done deal. The Japanese economy is not out of the woods yet – and there can certainly be no return to its pre-1990 boom years. The world has changed, as has Japan. Most of all, it has aged. Nearly 30% of the population is over 65 and the average age has risen from 37.2 in 1989 to 48.9 now. A shrinking and aging population is creating labour shortages throughout the economy and putting a real ceiling on growth. However, this demographic challenge is nothing new – nor is it unique to Japan. Japanese companies have been dealing with this for years, turning to increased automation, offshoring, and immigrant labour. This experience may even prove a competitive advantage, as more and more countries take the same greying path – from developed Europe to still-developing China.

It nonetheless keeps the structural risk of a return of deflation in place. The BoJ has been careful not to declare the inflation fight won yet. Although the yen has continued to weaken against the dollar despite the BoJ’s tightening, there is a risk that a strengthening yen could push some international investors away, hitting Japanese stocks. But for all these caveats, Japanese equities retain plenty of value to unlock – and real progress finally seems to be being made.

Click here to go back to Asia Overview

If you would like to find out more about these this theme or how you can take advantage of the current climate, please get touch with info@bedrockgroup.ch.

Authored by:

Important Legal Information

The content of this document has been prepared by Bedrock S.A., Bedrock Monaco SAM, and Bedrock Asset Management (UK) Ltd. (jointly, hereafter, “Bedrock”).

The information and opinions contained in this document are for background information and discussion purposes only and do not purport to be full or complete. No information in this document should be construed as providing financial, investment or other professional advice.

The information contained herein is intended for the sole use of the recipient and may not be copied or otherwise distributed or published without the express consent of Bedrock. Although the information contained herein has been established by Bedrock based on or by reference to sources, documents and systems it believes to be reliable and accurate, Bedrock does not guarantee its accuracy or completeness and assumes no responsibility for any losses that may arise from the use of this information.

Information included in this document is intended for those investors who meet the definition of Professional Client under the Swiss FinSA regulation as well as Professional Client or Eligible Counterparty under the UK Financial Conduct Authority.

Confidentiality

This presentation and the information contained herein are confidential. Each copy of this presentation is addressed to a specifically named recipient and shall not be passed on to a third party. By its acceptance hereof, the recipient agrees to keep the presentation and its contents strictly confidential and may not disclose or divulge any information contained herein to any other person. This presentation cannot be published, copied, reproduced or distributed in any manner whatsoever. The recipient will use this presentation for the sole purpose of obtaining a general understanding of the business, operations and financial performance of Bedrock in order to make a decision as to whether the recipient should proceed with a further investigation of the Funds and this investment opportunity. Bedrock reserves the right to request the return of this presentation at any time, without the retention of any copies by the prospective investor.

Investment Risks The value of all investments and the income derived therefrom can fluctuate due to market movements and you may not get back the amount originally invested. In the case of overseas investments, values may vary as a result of changes in currency exchange rates. This may be due, in part, to exchange rate fluctuations in investments that have an exposure to currencies other than the

base currency of the portfolio. Past performance is no guide to or guarantee of future performance.

Limitation of Liability and Indemnity

Bedrock expressly disclaims liability for errors or omissions in the information and data contained in this document. No representation or warranty of any kind, implied, expressed or statutory, is given in conjunction with the information and data. Bedrock accepts no liability for any loss or damage arising out of the use or misuse of or reliance on the information provided including, without limitation, any loss of profits or any other damage, direct or consequential. You agree to indemnify and hold harm less Bedrock and its affiliates, and the directors and employees of Bedrock and its affiliates from and against any and all liabilities, claims, damages, losses or expenses, including legal fees and expenses arising out of your access to or use of the information in this presentation, save to the extent that such losses may not be excluded pursuant to applicable law or regulation. Any opinions contained in this presentation may be changed after issue at any time without notice.

Copyright and Other Rights

The copyright, trademarks and all similar rights of this presentation and the contents, including all information, graphics, code, text and design, are owned by Bedrock.

This month, we discuss the Fed's closer-than-expected hold, the bear-steepening it triggered, and the forced deleveraging that amplified an AI-driven selloff.

Emerging market equities have delivered strong performance in 2026, fuelled by surging demand for AI-related technologies and significant gains across North Asian markets. In this article, Bedrock's Head of Investment Advisory, Helena Eaton, explores the key drivers behind this rally and the opportunities that may lie ahead.

This month we discuss an Iran ceasefire that finally won its signatures and the oil unwind that followed, Kevin Warsh’s first meeting at the Fed and the real-rate squeeze it set off, a blockbuster SpaceX debut that soared then drifted, and a memory shortage that turned an Asian semiconductor selloff into a story about demand, with a change of government in Britain and the ECB’s first hike in two years rounding out a busy month.